Wondering if Cedar Financial can affect your credit score?

Here’s the straightforward answer: any credit reporting on a personal account is carried out by Cedars Business Services on behalf of the original creditor.

The entry that appears on your credit report comes from Cedars Business Services as the furnisher, but it also reflects the original creditor’s name and account details — so both pieces of information sit side by side on the report.

That’s an important distinction, because it means that the entry you might see on a credit report might contain an unfamiliar name, such as Cedars Business Services, since they are the ones reporting a delinquent account on behalf of the original creditor.

Understanding how it all works – and why two Cedar-named brands come up in the same conversation – is the best way to replace confusion with clarity.

This guide walks you through exactly how credit reporting works in a collections context, how these two entities fit together, and what practical steps to take if you ever need to verify or dispute an account.

Cedar Financial and Cedars Business Services: Same Group, Different Roles

Cedar Financial and Cedars Business Services are related companies that operate under the same parent organization, Cedar Holdings International, Inc.

They are not two separate, unrelated businesses – but they are also not two names for the same thing. Each brand has a clearly defined role, and understanding which one does what is the foundation for answering any credit score question accurately.

Cedar Financial

A business-to-business (B2B), business-facing brand that provides fintech and end-to-end account receivables management (ARM) solutions to companies. Its clients are businesses and creditors, not individual consumers. Cedar Financial itself does not contact consumers directly and is not the name that would appear on a personal credit report.

Cedars Business Services

The consumer-facing, licensed collection arm of the group. This is the entity authorized to communicate with consumers about specific accounts, carry out collection efforts in compliance with applicable laws, and – where appropriate – furnish account information to the credit bureaus on behalf of the original creditor.

Cedar Holdings International

The parent organization that both brands sit under. Knowing this shared parent exists explains why the names appear related in search results – because they are.

Confusion happens for understandable reasons. The names sound alike, search engines often blend branded queries together, and online forums tend to use “Cedar” as a catch-all shorthand. When someone is stressed about a phone call or letter, it is easy to assume every “Cedar” mention applies to them in the same way – but that assumption can lead to the wrong conclusions about what is actually happening with their account or credit.

Before worrying about credit impact, take a moment to confirm which entity is actually contacting you. Check any letter, voicemail, or email for the full legal name, mailing address, and official contact details. That single step removes most of the guesswork.

Beyond the basics, there are a few specific markers worth checking – the kind of details scammers tend to get wrong and legitimate communications consistently get right. Our blog, Real vs Fake Cedar: How to Verify Legitimate Cedars Business Services Communication walks through them.

How Debt Collection Can Impact Your Credit Score

To understand whether collection activity could affect your credit, it helps to know how debt collection and credit reporting actually interact – and why timing matters so much.

The delinquency clock starts before collections

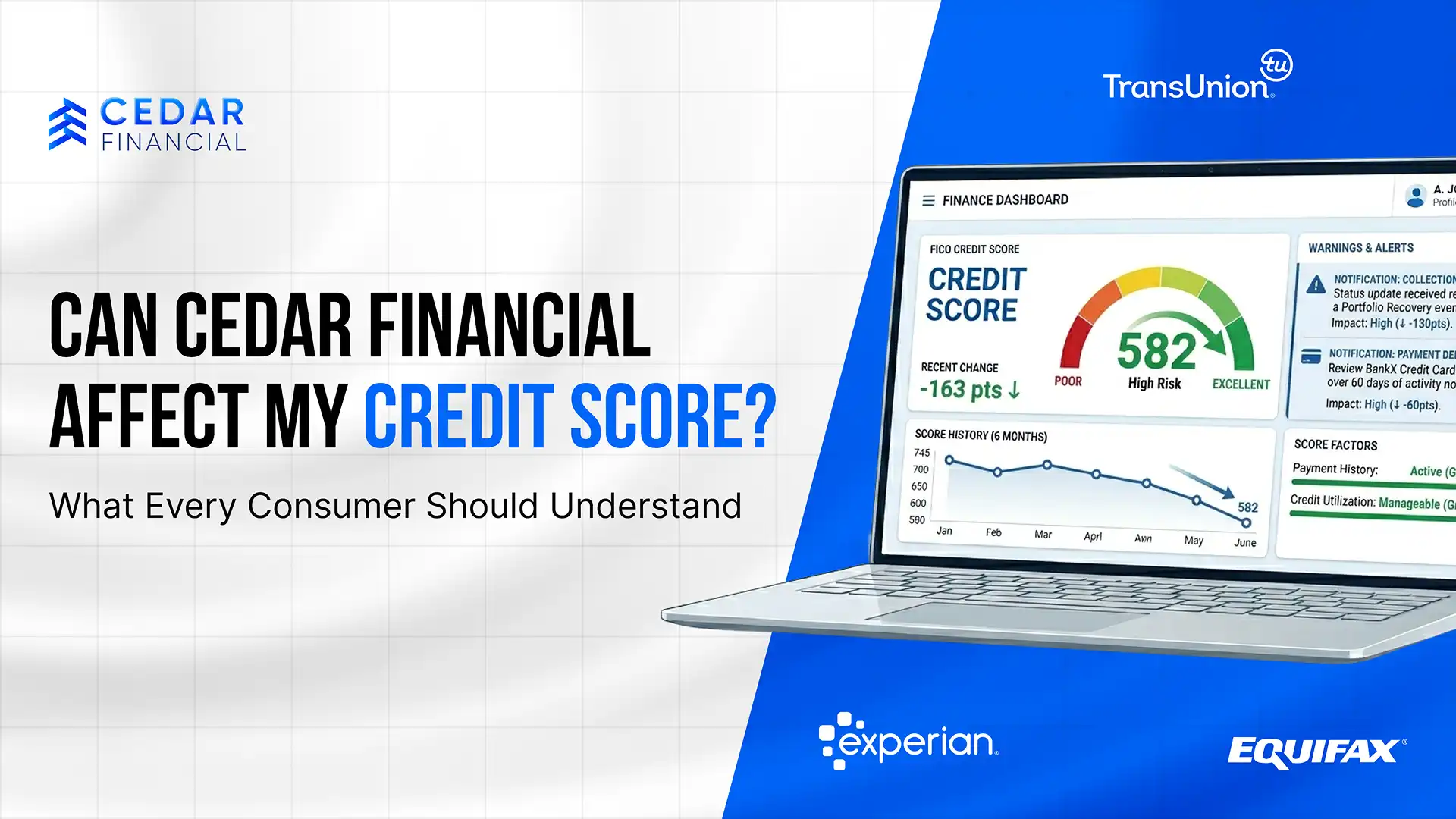

Credit impact typically begins long before an account reaches a collection agency. A payment is generally considered delinquent once it is 30 days past due, and that initial 30-day late mark is usually reported by the original creditor – not by a collection agency. Payment history is the single largest factor in a FICO score, accounting for roughly 35% of the calculation, which is why even one 30-day delinquency can cause a noticeable drop.

The hit tends to be sharper for consumers with higher scores to begin with. Industry analysts note that a single 30-day delinquency can cost a near-perfect score 100 points or more, while consumers with already-lower scores typically see smaller point drops. In other words, the higher you start, the farther you can fall from a single missed payment.

What a collection account is

If an account remains unpaid as it ages – commonly passing 60, 90, and 180 days past due – the original creditor may place or sell the account to a third-party collection agency. A collection account is a separate notation on a credit report that indicates a past-due debt has been placed with, or sold to, a third party for recovery. It is distinct from the original tradeline, though both may appear on the report.

The role of collection agencies in credit reporting

Third-party collection agencies may furnish information to the credit bureaus, but only under specific conditions and in line with federal consumer protection laws such as the Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA).

Any information that is reported must be accurate, verifiable, and tied to a legitimate account – and consumers retain the right to dispute anything that isn’t.

Does Cedars Business Services Report Accounts to Credit Bureaus?

A natural follow-up question is: does Cedars Business Services report accounts to credit bureaus?

As a licensed third-party collection agency, it may report certain accounts to one or more of the major credit bureaus – Equifax, Experian, and TransUnion – but this is not automatic for every account it handles.

When reporting does occur, Cedars Business Services acts as the furnisher on behalf of the original creditor. That means the credit report entry identifies both Cedars Business Services (as the collector reporting the information) and the original creditor (along with the underlying account details).

Whether a specific account is reported at all usually depends on factors such as:

· The original creditor’s reporting instructions and policies.

· The type and age of the debt.

· Whether the account has completed certain pre-reporting steps, such as validation notices.

· Applicable state and federal laws governing how and when collections data may be furnished.

The Key Takeaway:

Not every account assigned to a collection agency is reported to the bureaus, and many are resolved before any reporting ever takes place. If you want to know whether a specific account has been reported, the most reliable approach is to check your credit reports directly rather than relying on online speculation.

When a Debt May Appear on Your Credit Report

Timing is one of the most misunderstood parts of the collections process. An overdue balance does not instantly become a collection entry on your credit file – there is a typical sequence of events that unfolds first.

Before collection: the original creditor’s reporting

While an account is still with the original creditor, late payments may be reported at the 30-, 60-, and 90-day past-due marks – but this is the creditor’s reporting, not a collection agency’s. Some lenders hold off until 60 or 90 days before reporting, while others begin at 30 days. At this stage, no third-party collection account exists yet.

After assignment to a collection agency

If the account remains unpaid, the creditor may eventually assign or sell it to a collection agency. At that point, a new entry – a collection account – may appear on your credit report, furnished by the agency on behalf of the creditor. Whether this happens depends on the agency’s and creditor’s policies, the account details, and applicable rules.

How long it stays on your credit report

Under federal law, most negative entries related to a delinquent account can remain on a credit report for up to seven years. For accounts that go to collections or are charged off, the seven-year clock generally starts 180 days after the original delinquency – and that start date doesn’t reset if the debt is later sold to a different collector or if partial payments are made.

The good news: the impact on a credit score fades over time. A three-year-old late payment typically weighs far less on a score than a fresh one, and positive payment activity added in the meantime helps rebuild the profile.

What to Do If You See a Collection Account on Your Credit Report

If you pull your credit report and notice a collection account – whether it references Cedars Business Services, another agency, or an unfamiliar creditor – try not to panic. Instead, move through a calm, structured set of steps.

Pull all three reports: Each of the major bureaus (Equifax, Experian, TransUnion) may have slightly different information. Federal law entitles you to a free report from each bureau at least once every 12 months via Annual Credit Report, and the bureaus currently offer free weekly online reports as well.

Verify the debt: Confirm the original creditor, the amount, and the dates. Make sure the account actually belongs to you. Studies have found that a meaningful

share of consumers discover errors on their reports – including accounts they don’t recognize – so verification matters.

Request validation: Under the FDCPA, you generally have the right to request written validation of a debt. This helps confirm that the agency is authorized to collect it and that the details are correct.

Dispute inaccuracies: If the information is wrong, outdated, or not yours, you have the right to dispute it with the credit bureau and the furnisher of the information. Simple factual errors can often be corrected, though the process can take weeks to several months.

Contact the appropriate party in writing: Reach out directly to the agency listed on the report. Keep communication in writing where possible, and save copies of everything.

Taking these steps methodically is far more effective than reacting based on fear or misinformation. It also creates a clear paper trail if you need to escalate anything later.

Another thing to note is that not every unfamiliar account is an error. Accounts change hands, company names shift, and old bills resurface in ways most people don’t expect – 4 Reasons Why You Might Not Recognize a Debt and What to Do Next covers the most common ones.

How to Protect Your Credit When Contacted About a Debt

Proactive behavior is one of the strongest ways to protect your credit. If you are contacted about a debt, a few simple habits can make a meaningful difference.

1. Respond Early

Ignoring collection calls or letters rarely improves the situation. Engaging before the account reaches later delinquency stages usually gives you more options — and a single on-time action can sometimes change the trajectory of the account.

2. Set Up Monitoring

Consider using a free credit monitoring service or the bureaus’ free weekly reports so you’re never surprised by what’s on your file. Spotting issues early makes them much easier to address.

3. Keep Records

Save copies of all letters, emails, and notes from phone calls, including dates, names, and reference numbers.

4. Understand Your Rights

You have protections under the FDCPA and the FCRA, including the right to dispute, request validation, and be treated respectfully and within the bounds of the law.

5. Avoid Misinformation

Be cautious with forums and social media threads that make sweeping claims about specific agencies. Your situation is specific to your account.

Staying organized and informed is almost always more useful than searching for worst-case scenarios online.

Why Online Information About Credit Impact Can Be Misleading

If you’ve been researching “can Cedar Financial affect my credit score,” you’ve probably seen a mix of sources – some helpful, many not. It’s worth understanding why so much of what appears online can be misleading.

Forum-based misinformation: Much of what people read on forums is one-sided, emotionally charged, and based on incomplete information about the original debt.

Lack of context in complaints: A complaint rarely includes the full picture – whether the debt was valid, whether notices were received, or whether the consumer used their rights to dispute.

SEO bias toward fear-based content: Search engines often surface dramatic or fear-driven posts because they get clicks, not because they are accurate. That does not mean they reflect your reality.

A better approach is to rely on reputable sources – the CFPB, the FTC, and the credit bureaus themselves — verify the specific entity that contacted you, and focus on the facts of your own account rather than anonymous online narratives. The credit impact question is just one piece of that larger misinformation problem. 5 Common Myths About Debt Collection Agencies addresses the other beliefs that routinely send consumers down the wrong path.

Key Takeaways About Cedar Financial and Credit Scores

To bring everything together, here are the most important points to remember:

Cedar Financial and Cedars Business Services are related entities operating under the same parent organization, Cedar Holdings International.

Cedar Financial is a B2B, business-facing brand providing fintech and ARM solutions to companies – it is not the entity that contacts individual consumers about personal debts.

Cedars Business Services is the licensed, consumer-facing collection arm. When it reports to the credit bureaus, it does so on behalf of the original creditor, and the entry reflects both Cedars Business Services as the furnisher and the original creditor’s name and account details.

Payment history drives roughly 35% of a FICO score, which is why the first 30-day delinquency – reported by the original creditor – is usually the point where credit impact begins.

Most negative entries can remain on a credit report for up to seven years, with the clock for collection accounts typically starting 180 days after the original delinquency.

Consumers have clear rights under the FDCPA and FCRA, including the right to validation and the right to dispute inaccurate information.

If you’re ever unsure, verify the identity of the entity contacting you and reach out through their official channels.

Frequently Asked Questions

Can Cedar Financial affect my credit score?

Does Cedars Business Services report to credit bureaus?

As a licensed third-party collection agency, Cedars Business Services may report certain accounts to the major credit bureaus — Equifax, Experian, and TransUnion — on behalf of the original creditor. However, not every account is reported. Whether an account is reported depends on the original creditor’s policies, the type of debt, the stage of collection, and applicable laws.

Will a collection account always appear on my credit report?

No. Not every unpaid debt becomes a collection entry on a credit report. Many accounts are resolved before any reporting occurs, and some creditors or agencies do not report certain types of accounts at all. Reporting is governed by specific rules rather than a blanket practice.

How long does a collection account stay on my credit report?

Under federal law, most negative entries — including collection accounts — can remain on a credit report for up to seven years. For accounts placed in collections or charged off, the seven-year clock generally starts 180 days after the original delinquency and does not reset if the debt is sold to another collector or if partial payments are made. The impact on your score does fade over time as the entry ages.

What should I do if I see Cedar on my credit report?

Start by identifying the exact name listed — typically this will be Cedars Business Services, since that is the consumer-facing entity. Review the account details carefully, compare them to the original creditor information shown, and verify whether the debt is yours. Then contact the listed agency in writing for clarification. You can also request debt validation and dispute any inaccurate information with the credit bureau.

Can I dispute a collection account?

Yes. Under the Fair Credit Reporting Act (FCRA), consumers have the right to dispute inaccurate, incomplete, or unverifiable information on their credit reports. You can file disputes directly with the credit bureau reporting the account and with the furnisher of the information. The investigation process can take anywhere from several weeks to several months, depending on the nature of the dispute.

How can I verify if a debt is legitimate?

Request a written debt validation notice from the collection agency. This typically includes the name of the original creditor, the amount owed, and your rights regarding the debt. If details do not match your records, you can dispute the debt and request further documentation before making any payment.

Helpful Resources

For neutral, authoritative information about your rights and credit reporting, these government and consumer resources are useful starting points:

- Consumer Financial Protection Bureau (CFPB) — guidance on debt collection and credit reporting.

- Federal Trade Commission (FTC) — consumer rights under the FDCPA and related laws.

- AnnualCreditReport — the only federally authorized source for free credit reports from all three bureaus.